The management of U is reviewing internal controls throughout the company. It has noted the following:-

1. In the trade receivables section, journal adjustments are made by the clerks, without any reference to their supervisor. Journal adjustments may relate to sales returns, discounts allowed, or transfers between accounts.

2. In the purchasing department, the purchasing manager selects and approves all suppliers, as they are the only person with sufficient experience to do so. They use a very limited number of suppliers because they can rely on these suppliers to provide goods of the quality required at a competitive price. They do not keep any documents in relation to negotiations with other potential suppliers or other quotes obtained.

In relation to the above, which of the following statements are valid?

You have been assigned the role of lead internal auditor. Your task is to carry out the annual assessment of the production line maintenance department.

When planning for this audit, which of the following must be completed?

Which of the following statements concerning the role of the Audit Committee is correct?

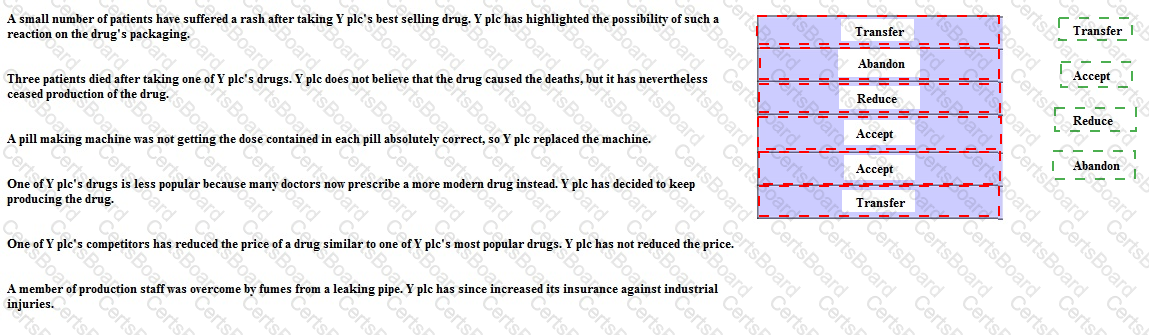

Y plc, a pharmaceutical company, has dealt with a number of risks in the manner indicated below.

Use the TARA framework to classify each of Y plc's responses.

TESTED 03 May 2024